There are two particularly good reads posted by Federal Reserve economists today. The first is "Deleveraging: Is it over and what was it?" by Claudia Sahm. The role of household deleveraging in the Great Recession has been heavily emphasized, notably at Atif Mian and Amir Sufi's very good new "House of Debt" blog. Sahm summarizes three new research papers on the topic of household deleveraging. The papers address three big questions:

- When will deleveraging be over?

- What do households do when they can't repay their debts?

- Whose decision is deleveraging anyway?

The research on Question 2 is especially interesting:

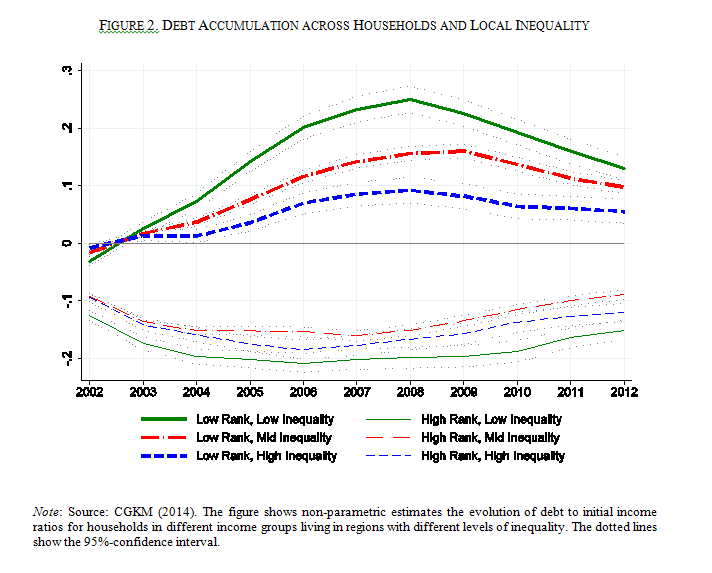

"Given the increase in mortgage defaults in this recession, it took unusually long (averaging up to 3 years in some states) to go from initial delinquency to a completed foreclosure on a home. During the foreclosure process, households typically lived 'rent free' in their homes. So what did these households do with the extra cash? The authors find a significant improvement in the performance of credit card debt (reduced delinquency and lower balances). Although these households were under considerable financial stress and were already facing a huge hit to their credit scores due to a foreclosure, they used some of the freed up money to pay off their other debts...Normally economists think that if you give cash to households who are financially constrained they will spend it not use it to service debt."Sahm's overall takeaway from the research she reviews is that:

"There was a big hit to 'permanent income' (households' expected lifetime income and net worth) and credit availability. Thus the level of spending and debt that made sense for households changed dramatically with the recession. Economists already understood this adjustment in the standard consumption framework even if the size and persistence of the shocks have been surprising. So in this sense "deleveraging" is simply a new way to frame the issue rather than a new behavior. And yet, we saw that the debt obligations that households made when everyone thought they were richer could not be easily undone."Another Fed post worth reading today is a speech, "A Review of the Experience of Fielding the Survey of Consumer Expectations," by James McAndrews. The New York Fed's Survey of Consumer Expectations (SCE) is a relatively new monthly survey of consumers' inflation, labor market, and household finance expectations.

The effort that the NY Fed has devoted to developing this survey is testament to the increasing emphasis economists are placing on understanding the links between expectations and the economy. (This is near and dear to me, as a theme of my dissertation.) Expectations have long played a role in macroeconomic models, but are sometimes treated as an afterthought, probably because they can be difficult to observe and quantify. The SCE includes probabilistic survey questions, which ask respondents to describe their probability distribution over future outcomes. This reveals the uncertainty associated with consumers' expectations.

In the speech, McAndrews delves into some of the nitty-gritty of the multi-year survey development process, which is quite fascinating. He also summarizes the past research using the survey data.