In recent months, there has been no notable change in inflation uncertainty at either horizon.

Consumers' inflation expectations are very disperse; on household surveys, many people report long-run inflation expectations that are far from the Fed's 2% target. Are these people unaware of the target, or do they know it but remain unconvinced of its credibility? In another paper in the Journal of Macroeconomics, I provide some non-experimental evidence that public knowledge of the Fed and its objectives is quite limited. In this paper, we directly treat respondents with information about the target and about past inflation, in randomized order, and see how they revise their reported long-run inflation expectations. We also collect some information about their prior knowledge of the Fed and the target, their self-reported understanding of inflation, and their numeracy and demographic characteristics. About a quarter of respondents knew the Fed's target and two-thirds could identify Yellen as Fed Chair from a list of three options.I gave a 90 minute econ seminar today with the twin babies, both awake. Held one and audience passed the other around. A first in economics?— Carola Conces Binder (@cconces) September 28, 2017

I show that several issues with estimates of information stickiness based on consumer survey microdata lead to substantial underestimation of the frequency with which consumers update their expectations. The first issue stems from data frequency. The rotating panel of Michigan Survey of Consumer (MSC) respondents take the survey twice with a six-month gap. A consumer may have the same forecast at months t and t+ 6 but different forecasts in between. The second issue is that responses are reported to the nearest integer. A consumer may update her information, but if the update results in a sufficiently small revisions, it will appear that she has not updated her information.To quantify how these issues matter, I use data from the New York Fed Survey of Consumer Expectations, which is available monthly and not rounded to the nearest integer. I compute updating frequency with this data. It is very high-- at least 5 revisions in 8 months, as opposed to the 1 revision per 8 months found in previous literature.

when I think about people who are hostile to capitalism, per se, I would argue that capitalism is not the problem. It's us. Capitalism is, what it's really good at, is giving us what we want--more or less...And so, if you want to change capitalism, you've got to change us. And that's--I really see that--I like the Pope doing that. I'm all for that.

It's mainly on the--the point we were talking about before, consuming too much. It's exhortation. He is basically saying what has been said by the Church for the last 2000 year...Look, you don't need all this stuff. It's pulling you away from the ultimate ends of your life. You are just pursuing it and not what you are meant, what you were created by God to pursue. You were created by God to pursue God, not to pursue this Mammon stuff.

|

| Source: http://voxeu.org/article/views-happiness-and-wellbeing-objectives-macroeconomic-policy |

"A unit of pleasure or pain is difficult even to conceive; but it is the amount of these feelings which is continually prompting us to buying and selling, borrowing and lending, labouring and resting, producing and consuming; and it is from the quantitative effects of the feelings that we must estimate their comparative amounts."Hence generations of economists have been trained in welfare economics based on utility theory, in which utility is an increasing function of consumption, u(c). Under neoclassical assumptions-- cardinal utility, stable preferences, diminishing marginal utility, and interpersonally comparable utility functions-- trying to maximize a social welfare function that is just the sum of all individual utility functions is totally Benthamite. And a focus on GDP growth is very natural, as more income should mean more consumption.

"Note that among Democrats, year-ahead income expectations fell and year-ahead inflation expectations rose, and among Republicans, income expectations rose and inflation expectations fell. Perhaps the most drastic shifts were in unemployment expectations:rising unemployment was anticipated by 46% of Democrats in December, up from just 17% in June, but for Republicans, rising unemployment was anticipated by just 3% in December, down from 41% in June. The initial response of both Republicans and Democrats to Trump’s election is as clear as it is unsustainable: one side anticipates an economic downturn, and the other expects very robust economic growth."This is from Richard Curtin, Director of the Michigan Survey of Consumers. He is comparing the economic sentiments and expectations of Democrats, Independents, and Republicans who took the survey in June and December 2016. A subset of survey respondents take the survey twice, with a six-month gap. So these are the respondents who took the survey before and after the election. The results are summarized in the table below, and really are striking, especially with regards to unemployment. Inflation expectations also rose for Democrats and fell for Republicans (and the way I interpret the survey data is that most consumers see inflation as a bad thing, so lower inflation expectations means greater optimism.)

|

| Source: Richard Curtin, Michigan Survey of Consumers |

|

| Source: December 5 FEDS Note |

"To carry out the executive power and be accountable for the exercise of that power, the President must be able to control subordinate officers in executive agencies. In its landmark decision in Myers v. United States, 272 U.S. 52 (1926), authored by Chief Justice and former President Taft, the Supreme Court therefore recognized the President’s Article II authority to supervise, direct, and remove at will subordinate officers in the Executive Branch.The decision goes on to add that "No head of either an executive agency or an independent agency operates unilaterally without any check on his or her authority. Therefore, no independent agency exercising substantial executive authority has ever been headed by a single person. Until now."

In 1935, however, the Supreme Court carved out an exception to Myers and Article II by permitting Congress to create independent agencies that exercise executive power. See Humphrey’s Executor v. United States, 295 U.S. 602 (1935). An agency is considered “independent” when the agency heads are removable by the President only for cause, not at will, and therefore are not supervised or directed by the President. Examples of independent agencies include well-known bodies such as the Federal Communications Commission, the Securities and Exchange Commission, the Federal Trade Commission, the National Labor Relations Board, and the Federal Energy Regulatory Commission... To help mitigate the risk to individual liberty, the independent agencies, although not checked by the President, have historically been headed by multiple commissioners, directors, or board members who act as checks on one another. Each independent agency has traditionally been established, in the Supreme Court’s words, as a “body of experts appointed by law and informed by experience."

"Some public policy decisions have -- or are perceived to have -- mostly general impacts, affecting most citizens in similar ways. Monetary policy, for example...is usually thought of as affecting the whole economy rather than particular groups or industries. Other public policies are more naturally thought of as particularist, conferring benefits and imposing costs on identifiable groups...When the issues are particularist, the visible hand of interest-group politics is likely to be most pernicious -- which would seem to support delegating authority to unelected experts. But these are precisely the issues that require the heaviest doses of value judgments to decide who should win and lose. Such judgments are inherently and appropriately political. It's a genuine dilemma."The Federal Reserve's Congressional mandate is to promote price stability and maximum employment. Federal Reserve independence is intended to promote these objectives by alleviating political pressure to pursue overly-accomodative monetary policy. Of course, as we have seen in recent years, the interest-group politics of central banking are more nuanced than a simple desire by incumbents for inflation. Interest rate policy and inflation affect different segments of the population in different ways. The CFPB is supposed to enforce federal consumer financial laws and protect consumers in financial markets. The average benefits of the CFPB to individual consumers is probably fairly small, while the costs of regulation and enforcement to a smaller number of financial companies is large. This asymmetry means that political pressure on a financial regulator like the CFPB (or on the Fed, in its regulatory role) is likely to come from the side of the financial institutions. In Blinder's logic, this confers a large value on the delegation of authority to technocrats, while at the same time raising the importance of accountability for political legitimacy.

|

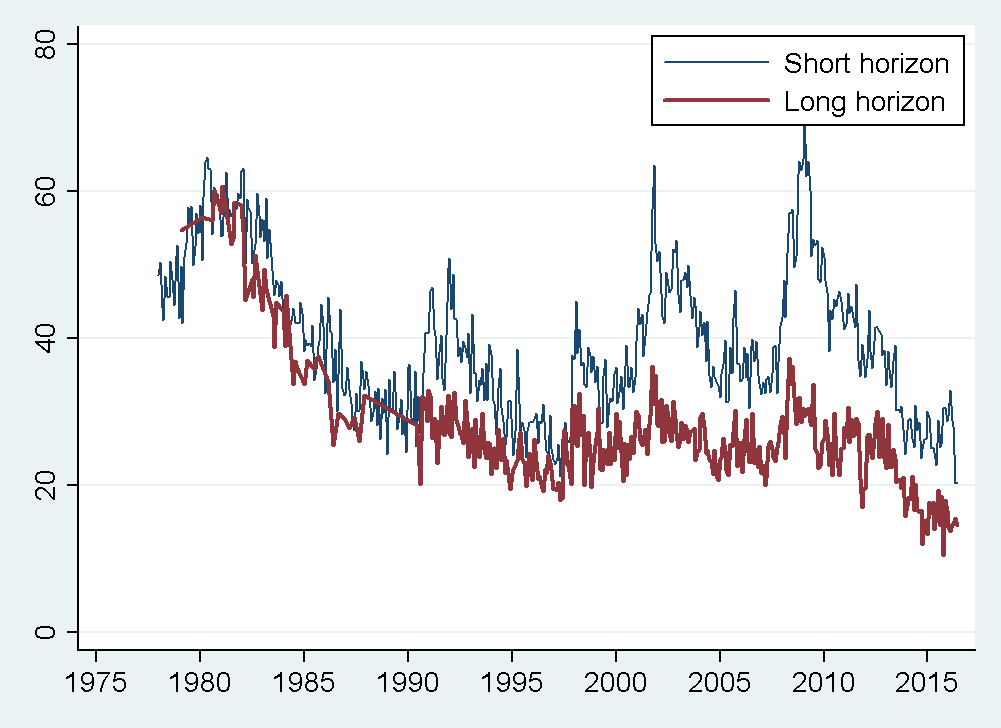

| Figure 1: Consumer inflation uncertainty index developed in Binder (2015) using data from the University of Michigan Survey of Consumers. To download updated data, visit https://sites.google.com/site/inflationuncertainty/. |

|

| Figure 2: Consumer inflation uncertainty index (centered 3-month moving average) developed in Binder (2015) using data from the University of Michigan Survey of Consumers. To download updated data, visit https://sites.google.com/site/inflationuncertainty/. |

|

| Figure 3: Created by Binder with data from University of Michigan Survey of Consumers |

"Congress has passed the Truth-in-Lending Act; the National Conference of Commissioners on Uniform State Laws has proposed the Uniform Consumer Credit Code; and many states have enacted retail installment sales acts to update and supplement their long-standing usury laws. These legislative and judicial acts have always relied, at best, on anecdotal knowledge of consumer behavior. In this Article we offer the results of an empirical study of a small slice of consumer behavior in the use of installment credit.

In their recent efforts, the legislatures, by imposing new interest rate disclosure requirements on installment lenders, have sought to protect the consumer against pressures to borrow money at a higher rate of interest than he can afford or need pay. The hope, if not the expectation, of the drafters of such disclosure legislation is that the consumer who is made aware of interest rates will seek the lowest-priced lender or will decide not to borrow. This migration of the consumers to the lowest-priced lender will, so the argument goes, require the higher-priced lender to reduce his rate in order to retain his business. These hopes and expectations are founded on the proposition that the consumer is largely ignorant of the interest rate that he pays; this ignorance presumably keeps him from going to a lender with cheaper rates. Knowledge of interest rates, it is believed, will rectify this defect…”

“Presumably, consumers in a perfect market will behave like water in a pond, which gravitates to the lowest point-i.e., consumer borrowers should all tum to the lender that gives the cheapest loan. We began this project with a strong suspicion-based on the observations of others-that the consumer credit market is far from perfect and that water governed by the force of gravity is a poor metaphor with which to describe the behavior of consumer debtors. The consumer debtor's choice of creditor clearly involves consideration of many factors besides interest rate. Therefore, a metaphor that better describes our suspicions about the borrower's behavior in a market in which rate differences appear involves a group of monkeys in a cage with a new baboon of unknown temperament. The baboon squats in one comer of the cage near some choice, ripe bananas. In the far comer of the cage is a supply of wilted greens and spoiled bananas, the monkeys' usual fare. Some of the monkeys continue eating their usual fare because they are unaware of the new bananas and the visitor. Other monkeys observe the new bananas but do not approach them. Still others, more daring or intelligent than the rest, seek ways of snatching an occasional banana from the baboon's stock. The baboon strikes at all the brown monkeys but he permits black monkeys to eat without interference. Yet many of the black monkeys make no attempt to eat. One suspects that a social scientist who interviewed the members of the monkey tribe about their experience would find that many of those who saw and appreciated the choice bananas would be unable to articulate the reasons for their failure to eat any of them. The social scientist might also discover that a few who looked at the baboon in obvious fright would nevertheless deny that they were afraid. In addition, he might find that some were so busy picking fleas or nursing that they did not observe the choice bananas at all. We suspected that consumer borrowers had similarly diverse reasons for their behavior.

We presumed that some paid high interest rates only because of ignorance of lower rates and that others correctly concluded that they could not qualify for a cheaper loan than they received. Others, we suspected, were merely too lazy or too fearful of bankers to seek lower rates.”

“The results of our study suggest that, at least with regard to auto loans, the disclosure provisions of the Truth-in-Lending Act will be largely ineffective in changing consumer behavior patterns. Certainly the Act will not improve the status of those who already know that lower rates are available elsewhere. And we discovered no evidence that knowledge of the interest rate-which, even under the Act will usually come after a tentative agreement to purchase a specified car has been reached-will stimulate a substantial percentage of consumers to shop for a lower rate elsewhere.”The authors come down as pessimistic about the Truth-in-Lending Act, but make no new policy recommendations of their own. If they were writing today, instead of just predicting that a policy would be ineffective, they might suggest ways to design the policy to "nudge" consumers to make different decisions. The Truth-in-Lending Act has been amended numerous times over the years, and was placed under the authority of the Consumer Financial Protection Bureau (CFPB) by the Dodd-Frank Act. Behavioral economics has played a central role in the work of the CFPB. But the active application of behavioral law and economics to regulatory policy is not universally accepted. For example, Todd Zwicki writes:

"We argue that even if the findings of behavioral economics are sound and robust, and the recommendations of behavioral law and economics are coherent (two heroic assumptions, especially the latter), there still remain vexing problems of actually implementing behavioral economics in a real-world political context. In particular, the realities of the political and regulatory process suggests that the trip from the laboratory to the real-world crafting of regulations that will improve consumers’ lives is a long and rocky one."Zwicki expands this argument in a paper coauthored with Adam Christopher Smith. While I'm not convinced that their rather negative portrayal of the CFPB is warranted, I do think the paper presents some provocative cautions about how behavioral economics is applied to policy--especially the warning against "selective modeling of behavioral bias," which I have heard even top behavioral economists caution against.

With respect to the risks to the inflation outlook, the most concerning is the possibility that inflation expectations become unanchored to the downside. This would be problematic were it to occur because inflation expectations are an important driver of actual inflation. If inflation expectations become unanchored to the downside, it would become much more difficult to push inflation back up to the central bank’s objective.Dudley, perhaps because of his New York Fed affiliation, pointed to the New York Fed’s Survey of Consumer Expectations as his preferred indicator of inflation expectations. He noted that on this survey, "The median of 3-year inflation expectations has declined over the past year, falling by 22 basis points to 2.8 percent. While the magnitude of this decline is small, I think it is noteworthy because the current reading is below where we have been during the survey history."

|

| Source: Data from Survey of Consumer Expectations, © 2013-2015 Federal Reserve Bank of New York (FRBNY). Calculations by Carola Binder. |

|

| Figure 1: Data from Michigan Survey of Consumers. Analysis by Binder. |

|

| Figure 2: Data from Michigan Survey of Consumers. Analysis by Binder. |

"The inflation expectations of high-income, college-educated, male, and working-age people play a larger role in inflation dynamics than do the expectations of other groups of consumers or of professional forecasters."Update: The permanent link to the paper is here.

"Among the traditional reasons proposed include increasing urbanization, a decline in public spirit, increasing time pressure, rising crime (this pattern reversed long ago), increasing concerns about privacy and confidentiality, and declining cooperation due to 'over-surveyed' households (Groves and Couper 1998; Presser and McCullogh 2011; Brick and Williams 2013). The continuing increase in survey nonresponse as urbanization has slowed and crime has fallen make these less likely explanations for present trends. Tests of the remaining hypotheses are weak, based largely on national time-series analyses with a handful of observations. Several of the hypotheses require measuring societal conditions that can be difficult to capture: the degree of public spirit, concern about confidentiality, and time pressure...We are unaware of strong evidence to support or refute a steady decline in public spirit or a rise in confidentiality concerns as a cause for declines in survey quality."They find it most likely that the sharp rise in the number of government surveys administered in the US since 1984 has resulted in declining cooperation by "over-surveyed" households. "We suspect that talking with an interviewer, which once was a rare chance to tell someone about your life, now is crowded out by an annoying press of telemarketers and commercial surveyors."