In recent months, there has been no notable change in inflation uncertainty at either horizon.

...The dollar rose and the 10-year U.S. Treasury note fell on Monday after Bloomberg News reported Taylor, a professor at Stanford University, impressed President Donald Trump in a recent White House interview.

Driving those trades was speculation that the 70 year-old Taylor would push rates up to higher levels than a Fed helmed by its current chair, Janet Yellen. That’s because he is the architect of the Taylor Rule, a tool widely used among policy makers as a guide for setting rates since he developed it in the early 1990s.But the second, by Rich Miller, claims that "Taylor’s Walk on Supply Side May Leave Him More Dove Than Yellen." Miller explains,

"While Taylor believes the [Trump] administration can substantially lift non-inflationary economic growth through deregulation and tax changes, Yellen is more cautious. That suggests that the Republican Taylor would be less prone than the Democrat Yellen to raise interest rates in response to a policy-driven economic pick-up."What actually makes someone a hawk? Simply favoring rules-based policy is not enough. A central banker could use a variation of the Taylor rule that implies very little response to inflation, or that allows very high average inflation. Beliefs about the efficacy of supply-side policies also do not determine hawk or dove status. Let's look at the Taylor rule from Taylor's 1993 paper:

r = p + .5y + .5(p – 2) + 2,where r is the federal funds rate, y is the percent deviation of real GDP from target, and p is inflation over the previous 4 quarters. Taylor notes (p. 202) that lagged inflation is used as a proxy for expected inflation, and y=100(Y-Y*)/Y* where Y is real GDP and Y* is trend GDP (a proxy for potential GDP).

“a welfarist analyzing tax policies that entail tradeoffs between efficiency and equity would not be far off in just looking at static distribution tables and ignoring any dynamic effects altogether. This is true for just about any social welfare function that places a greater weight on absolute gains for households at the bottom than at the top. Under such an approach policymaking could still be done under a lexicographic process—so two tax plans with the same distribution would be evaluated on the basis of whichever had higher growth rates…but in this case growth would be the last consideration, not the first” (16).

Consumers' inflation expectations are very disperse; on household surveys, many people report long-run inflation expectations that are far from the Fed's 2% target. Are these people unaware of the target, or do they know it but remain unconvinced of its credibility? In another paper in the Journal of Macroeconomics, I provide some non-experimental evidence that public knowledge of the Fed and its objectives is quite limited. In this paper, we directly treat respondents with information about the target and about past inflation, in randomized order, and see how they revise their reported long-run inflation expectations. We also collect some information about their prior knowledge of the Fed and the target, their self-reported understanding of inflation, and their numeracy and demographic characteristics. About a quarter of respondents knew the Fed's target and two-thirds could identify Yellen as Fed Chair from a list of three options.I gave a 90 minute econ seminar today with the twin babies, both awake. Held one and audience passed the other around. A first in economics?— Carola Conces Binder (@cconces) September 28, 2017

I show that several issues with estimates of information stickiness based on consumer survey microdata lead to substantial underestimation of the frequency with which consumers update their expectations. The first issue stems from data frequency. The rotating panel of Michigan Survey of Consumer (MSC) respondents take the survey twice with a six-month gap. A consumer may have the same forecast at months t and t+ 6 but different forecasts in between. The second issue is that responses are reported to the nearest integer. A consumer may update her information, but if the update results in a sufficiently small revisions, it will appear that she has not updated her information.To quantify how these issues matter, I use data from the New York Fed Survey of Consumer Expectations, which is available monthly and not rounded to the nearest integer. I compute updating frequency with this data. It is very high-- at least 5 revisions in 8 months, as opposed to the 1 revision per 8 months found in previous literature.

The standard procedure in such cases is to assume that the quality-adjusted inflation rate is the same as for other items in the same category that the statistical office can follow over time, i.e. products that are not subject to creative destruction. However, creative destruction implies that the new products enter the market because they have a lower quality-adjusted price. Our study tries to quantify the bias that arises from relying on imputation to measure US productivity growth in cases of creative destruction.

If the statistical office is correct to assume that the quality-adjusted inflation rate is the same for creatively destroyed products as for surviving incumbent products, then the market share of surviving incumbent products should stay constant over time. If instead the market share of these incumbent products shrinks systematically over time, then the surviving subset of products must have higher average inflation than creatively destroyed products. For a given elasticity of substitution between products, the more the market share shrinks for surviving products, the more the missing growth.

Policymakers must be willing to rigorously assess the costs and benefits of previously-accepted policy parameters in response to economic changes. One of these key parameters that should be rigorously reassessed is the very low inflation targets that have guided monetary policy in recent decades. We believe that the Fed should appoint a diverse and representative blue ribbon commission with expertise, integrity, and transparency to evaluate and expeditiously recommend a path forward on these questions.

It took me a moment--and I'd guess I'm not alone--to even recognize how remarkable this is. The New York Times ran an article with the headline "Fed Officials Confront New Reality: Low Inflation and Low Unemployment." Confront, not embrace, not celebrate.I expect the FOMC minutes to reveal that some participants were concerned about low inflation while others focused on low unemployment.— Tim Duy (@TimDuy) August 16, 2017

And why the puzzlement at the failure of core inflation to rise to 2%? That is a puzzle only if you assume that you know with certainty that the unemployment rate is the right variable to put on the right hand side of the Phillips Curve. If you say that the right variable is equal to some combination with weight λ on prime-age employment-to-population and weight 1-λ on the unemployment rate, then there is no puzzle—there is simply information about what the current value of λ is.It is not totally obvious why prime-age employment-to-population should drive inflation distinctly from unemployment--that is, why Delong's λ should not be zero, as in the standard Phillips Curve. Note that the employment-to-population ratio grows with the labor force participation rate (LFPR) and declines with the unemployment rate. Typically, labor force participation is mostly acyclical: its longer run trends dwarf any movements at the business cycle frequency (see graph below). So in a normal recession, the decline in the employment-to-population ratio is mostly attributable to the rise in the unemployment rate, not the fall in LFPR (so it shouldn't really matter if you simply impose λ=0).

|

| https://fred.stlouisfed.org/series/LNS11300060 |

cyclical factors can fully account for the post-2007 decline of 1.5 percentage points in the LFPR for prime-age adults (i.e., 25–54 years old). We define the labor force participation gap as the deviation of the LFPR from its potential path implied by demographic and structural considerations, and we find that as of mid-2013 this gap stood at around 2%. Indeed, our analysis suggests that the labor force gap and the unemployment gap each accounts for roughly half of the current employment gap, that is, the shortfall of the employment-to-population rate from its precrisis trend.Erceg and Levin discuss their results in the context of the Phillips Curve, noting that "a large negative participation gap induces labor force participants to reduce their wage demands, although our calibration implies that the participation gap has less influence than the unemployment rate quantitatively." This means that both unemployment and labor force participation enter the right hand side of the Phillips Curve (and Delong's λ is nonzero), so if a deep recession leaves the LFPR (and, accordingly, the employment-to-population ratio) low even as unemployment returns to its natural rate, inflation will still remain low.

We use our model to analyze the implications of alternative monetary policy strategies against the backdrop of a deep recession that leaves the LFPR well below its longer run potential level. Specifically, we compare a noninertial Taylor rule, which responds to inflation and the unemployment gap to an augmented rule that also responds to the participation gap. In the simulations, the zero lower bound precludes the central bank from lowering policy rates enough to offset the aggregate demand shock for some time, producing a deep recession; once the shock dies away sufficiently, policy responds according to the Taylor rule. A key result of our analysis is that monetary policy can induce a more rapid closure of the participation gap through allowing the unemployment rate to fall below its longrun natural rate. Quite intuitively, keeping unemployment persistently low draws cyclical nonparticipants back into labor force more quickly. Given that the cyclical nonparticipants exert some downward pressure on inflation, some undershooting of the long-run natural rate actually turns out to be consistent with keeping inflation stable in our model.While the authors don't explicitly use the phrase "full employment," their paper does provide a rationale for the low core inflation we're experiencing despite low unemployment. Erceg and Levin's paper was published in the Journal of Money, Credit, and Banking in 2014; ungated working paper versions from 2013 are available here.

"Note that among Democrats, year-ahead income expectations fell and year-ahead inflation expectations rose, and among Republicans, income expectations rose and inflation expectations fell. Perhaps the most drastic shifts were in unemployment expectations:rising unemployment was anticipated by 46% of Democrats in December, up from just 17% in June, but for Republicans, rising unemployment was anticipated by just 3% in December, down from 41% in June. The initial response of both Republicans and Democrats to Trump’s election is as clear as it is unsustainable: one side anticipates an economic downturn, and the other expects very robust economic growth."This is from Richard Curtin, Director of the Michigan Survey of Consumers. He is comparing the economic sentiments and expectations of Democrats, Independents, and Republicans who took the survey in June and December 2016. A subset of survey respondents take the survey twice, with a six-month gap. So these are the respondents who took the survey before and after the election. The results are summarized in the table below, and really are striking, especially with regards to unemployment. Inflation expectations also rose for Democrats and fell for Republicans (and the way I interpret the survey data is that most consumers see inflation as a bad thing, so lower inflation expectations means greater optimism.)

|

| Source: Richard Curtin, Michigan Survey of Consumers |

|

| Source: December 5 FEDS Note |

"We find that depending on our calibration of the average duration and the unconditional frequency of ZLB episodes, the optimal inflation rate can range from 1.5% to 4%. This uncertainty stems ultimately from the paucity of historical experience with ZLB episodes, which makes pinning down these parameters with any degree of confidence very difficult. A key conclusion of the paper is therefore that much humility is called for when making recommendations about the optimal rate of inflation since this fundamental data constraint is unlikely to be relaxed anytime soon."The second paper, by Emi Nakamura, Jón Steinsson, Patrick Sun, and Daniel Villar, is called "The Elusive Costs of Inflation: Price Dispersion during the U.S. Great Inflation." This paper notes that in standard New Keynesian models with Calvo pricing, one of the main welfare costs of inflation comes from inefficient price dispersion. When inflation is high, prices get further from optimal between price resets. This distorts the allocative role of prices, as relative prices no longer accurately reflect relative costs of production. In a standard New Keynesian model, the implied cost of this reduction in production efficiency is about 10% if you move from 0% inflation to 12% inflation. This is huge-- an order of magnitude greater than the welfare costs of business cycle fluctuations in output. This is why standard models recommend a very low inflation target.

|

| Figure 1: Consumer inflation uncertainty index developed in Binder (2015) using data from the University of Michigan Survey of Consumers. To download updated data, visit https://sites.google.com/site/inflationuncertainty/. |

|

| Figure 2: Consumer inflation uncertainty index (centered 3-month moving average) developed in Binder (2015) using data from the University of Michigan Survey of Consumers. To download updated data, visit https://sites.google.com/site/inflationuncertainty/. |

|

| Figure 3: Created by Binder with data from University of Michigan Survey of Consumers |

Abstract: Expected inflation is a central variable in economic theory. Economic historians have estimated historical inflation expectations for a variety of purposes, including studies of the Fisher effect, the debt deflation hypothesis, central bank credibility, and expectations formation. I survey the statistical, narrative, and market-based approaches that have been used to estimate inflation expectations in historical eras, including the classical gold standard era, the hyperinflations of the 1920s, and the Great Depression, highlighting key methodological considerations and identifying areas that warrant further research. A meta-analysis of inflation expectations at the onset of the Great Depression reveals that the deflation of the early 1930s was mostly unanticipated, supporting the debt deflation hypothesis, and shows how these results are sensitive to estimation methodology.This paper is part of a new "Surveys and Speculations" feature in Explorations in Economic History. Recent volumes of the journal open with a Surveys and Speculations article, where "The idea is to combine the style of JEL [Journal of Economic Literature] articles with the more speculative ideas that one might put in a book – producing surveys that can help to guide future research. The emphasis can either be on the survey or the speculation part." Other examples include "What we can learn from the early history of sovereign debt" by David Stasavage, "Urbanization without growth in historical perspective" by Remi Jedwab and Dietrich Vollrath, and "Surnames: A new source for the history of social mobility" by Gregory Clark, Neil Cummins, Yu Hao, and Dan Diaz Vidal. The referee and editorial reports were extremely helpful, so I really recommend this if you're looking for an outlet for a JEL-style paper with economic history relevance.

“The hallmark of the new narrative is to think of medium- and longer-term macroeconomic outcomes in terms of regimes. The concept of a single, long-run steady state to which the economy is converging is abandoned, and is replaced by a set of possible regimes that the economy may visit. Regimes are generally viewed as persistent, and optimal monetary policy is viewed as regime dependent. Switches between regimes are viewed as not forecastable.”Bullard describes three “fundamentals” that characterize which regime the economy is in: productivity growth (high or low), the real return on short-term government debt (high or low), and state of the business cycle (recession or not). We are currently in a low-productivity growth, low rate, no-recession regime. The St. Louis Fed’s forecasts for the next 2.5 years are made with the assumption that we will stay in such a regime over the forecast horizon. They forecast real output growth of 2%, 4.7% unemployment, and 2% trimmed-mean PCE inflation.

"In an interesting application of robust control methods, Sargent (1999) studies a simple macro-policy model and shows that robustness, in the “robust control” sense, does not necessarily lead to policy attenuation. Instead, the robust policy rule may respond more aggressively to shocks. The intuition for this result is that, by pursuing a more aggressive policy, the central bank can prevent the economy from encountering situations where model misspecification might be especially damaging."In Bullard's Figure 1 (below), we see the baseline forecast corresponding to continuation in the no recession, low real rate of return, low productivity growth regime. We also see some of the upside risks to the policy rate path, corresponding to switches to high real rate of return and/or high productivity growth regimes. We also see the arrow pointing to recession, but the four possible outcomes associated with that switch are omitted from the diagram. Bullard writes that "We are currently in a no recession state, but it is possible that we could switch to a recession state. If such a switch occurred, all variables would be affected but most notably, the unemployment rate would rise substantially. Again, the possibility of such a switch does not enter directly into the forecast because we have no reason to forecast a recession given the data available today. The possibility of recession is instead a risk to the forecast."

With respect to the risks to the inflation outlook, the most concerning is the possibility that inflation expectations become unanchored to the downside. This would be problematic were it to occur because inflation expectations are an important driver of actual inflation. If inflation expectations become unanchored to the downside, it would become much more difficult to push inflation back up to the central bank’s objective.Dudley, perhaps because of his New York Fed affiliation, pointed to the New York Fed’s Survey of Consumer Expectations as his preferred indicator of inflation expectations. He noted that on this survey, "The median of 3-year inflation expectations has declined over the past year, falling by 22 basis points to 2.8 percent. While the magnitude of this decline is small, I think it is noteworthy because the current reading is below where we have been during the survey history."

|

| Source: Data from Survey of Consumer Expectations, © 2013-2015 Federal Reserve Bank of New York (FRBNY). Calculations by Carola Binder. |

"The inflation expectations of high-income, college-educated, male, and working-age people play a larger role in inflation dynamics than do the expectations of other groups of consumers or of professional forecasters."Update: The permanent link to the paper is here.

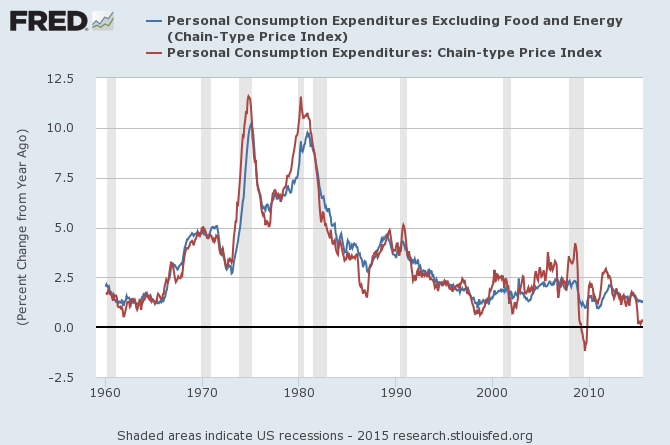

"Various monetary proposals can be viewed as inflation targeting with a nonstandard price index: The gold standard uses only the price of gold, and a fixed exchange rate uses only the price of a foreign currency."That's from a 2003 paper by Greg Mankiw and Ricardo Reis called "What Measure of Inflation Should a Central Bank Target?" At the time, the Federal Reserve had not explicitly announced its inflation target, though an emphasis on core inflation, which excludes volatile food and energy prices (the blue line in the figure below), arose under Alan Greenspan's chairmanship. Other central banks, including the Bank of England and the European Central Bank, instead focus on headline inflation. In 2012, the Fed formalized PCE inflation as its price stability target, but closely monitors core inflation as a key indicator of underlying inflation trends.. Some at the Fed, including St. Louis Fed President James Bullard, have argued that the Fed should focus more on headline inflation (the red line) and less on core inflation (the blue line).

|

| Source: FRED |

"One immediate benefit of dropping the emphasis on core inflation would be to reconnect the Fed with households and businesses who know price changes when they see them. With trips to the gas station and the grocery store being some of the most frequent shopping experiences for many Americans, it is hardly helpful for Fed credibility to appear to exclude all those prices from consideration in the formation of monetary policy."Bullard's concern is that since food and energy prices are so visible and salient for consumers, they might play an oversized role in perceptions and expectations of inflation. If the Fed holds core inflation steady while gas prices and headline inflation rise, maybe inflation expectations will rise a lot, becoming unanchored, and causing feedback into core inflation. There is mixed evidence on whether this is a real concern in recent years. I'm doing some work on this topic myself, and hope to share results soon.