"Various monetary proposals can be viewed as inflation targeting with a nonstandard price index: The gold standard uses only the price of gold, and a fixed exchange rate uses only the price of a foreign currency."

That's from a

2003 paper by Greg Mankiw and Ricardo Reis called "

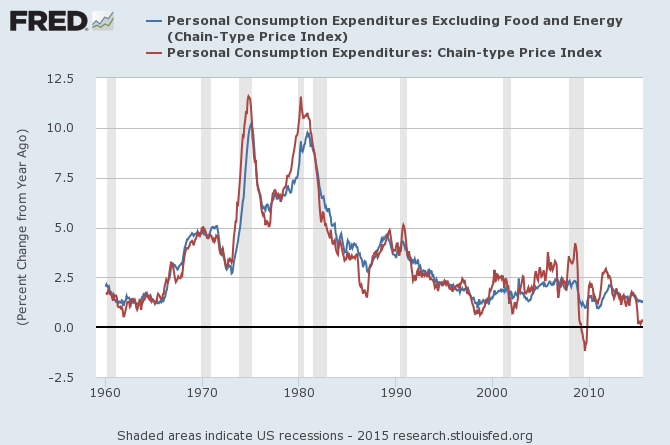

What Measure of Inflation Should a Central Bank Target?" At the time, the Federal Reserve had not explicitly announced its inflation target, though an emphasis on core inflation, which excludes volatile food and energy prices (the blue line in the figure below),

arose under Alan Greenspan's chairmanship. Other central banks, including the Bank of England and the European Central Bank, instead focus on headline inflation. In 2012, the Fed formalized PCE inflation as its price stability target, but closely monitors core inflation as a key indicator of underlying inflation trends.. Some at the Fed, including St. Louis Fed President James Bullard,

have argued that the Fed should focus more on headline inflation (the red line) and less on core inflation (the blue line).

Mankiw and Reis frame the issue more generally than just a choice between core and headline inflation. A price index assigns weights to prices in each sector of the economy. A core price index would put zero weight on food and energy prices, for example, but you could also construct a price index that put a weight of 0.75 on hamburgers and 0.25 on milkshakes, if that struck your fancy. Mankiw and Reis ask how a central bank can optimally choose these weights for the price index it will target in order to maximize some objective.

In particular, they suppose the central bank's objective is to minimize the volatility of the output gap. They explain, "We are interested in finding the price index that, if kept on an assigned target, would lead to the greatest stability in economic activity. This concept might be called the stability price index." They model how the weight on each sector in this stability price index depend on certain sectoral properties: the cyclical sensitivity of the sector, the proclivity of the sector to experience idiosyncratic shocks, and the speed with which the prices in the sector can adjust.

The findings are mostly intuitive. If a particular sector's prices are very procyclical, do not experience large idiosyncratic shocks, or are very sticky, that sector should receive relatively large weight in the stability price index. Each of these characteristics makes the sector more useful from a signal-extraction perspective as an indicator of economic activity.

Next, Mankiw and Reis do a "back-of-the-envelop" exercise to calculate the weights for a stability price index for the United States using data from 1957 to 2001. They consider four sectors: food, energy, other goods and services, and nominal wages. They stick to four sectors for simplicity, but it would also be possible to include other prices, like gold and other asset prices. To the extent that these are relatively flexible and volatile, they would probably receive little weight. The inclusion of nominal wages is interesting, because it is a price of labor, not of a consumption good, so it gets a weight of 0 in the consumer price index. But nominal wages are procyclical, not prone to indiosyncratic shocks, and sticky, so the result is that the stability price index weight on nominal wages is near one, while the other sectors get weights near zero. This finding is in line with

other results, even derived from very different models, about the optimality of including nominal wages in the monetary policy target.

More recently, Josh Bivens and others have

proposed nominal wage targets for monetary policy, but they frame this as an alternative to unemployment as an indicator of labor market slack for the full employment component of the Fed's mandate. In Mankiw and Reis' paper, even a strict inflation targeting central bank with no full employment goal may want to use nominal wages as a big part of its preferred measure of inflation. (Since productivity

If we leave nominal wages out of the picture, the results provide some justification for a focus on core, rather than headline, inflation. Namely, food and energy prices are very volatile and not very sticky. Note, however, that the paper assumes that the central bank has perfect credibility, and can thus achieve whatever inflation target it commits to. In

Bullard's argument against a focus on core inflation, he implicitly challenges this assumption:

"One immediate benefit of dropping the emphasis on core inflation would be to reconnect the

Fed with households and businesses who know price changes when they see them. With trips

to the gas station and the grocery store being some of the most frequent shopping experiences

for many Americans, it is hardly helpful for Fed credibility to appear to exclude all those prices

from consideration in the formation of monetary policy."

Bullard's concern is that since food and energy prices are so visible and salient for consumers, they

might play an

oversized role in perceptions and expectations of inflation. If the Fed holds core inflation steady while gas prices and headline inflation rise, maybe inflation expectations will rise a lot, becoming unanchored, and causing

feedback into core inflation. There is

mixed evidence on whether this is a real concern in recent years. I'm doing some work on this topic myself, and hope to share results soon.

As an aside to my students in Senior Research Seminar, I highly recommend the Mankiw and Reis paper as an example of

how to write well, especially if you plan to do a theoretical thesis.

Note: The description of the Federal Reserve's inflation target in the first paragraph of this post was edited for accuracy on September 25.