TIPS have a surprisingly interesting history, one that is both longer and shorter than you might expect. Though inflation-indexed bonds made a brief-lived appearance in Massachusetts in 1780, they then disappeared for more than two centuries. TIPS were not issued until 1997, at the urging of then Treasury Secretary Robert Rubin. This is the first of a series of posts I will write about inflation-indexed securities. In this post, I describe their history. In future posts I will review the evidence on whether TIPS have lived up to Rubin's claims that they would benefit savers and reduce the government's borrowing costs, as well as exploring other implications of this teenage asset.

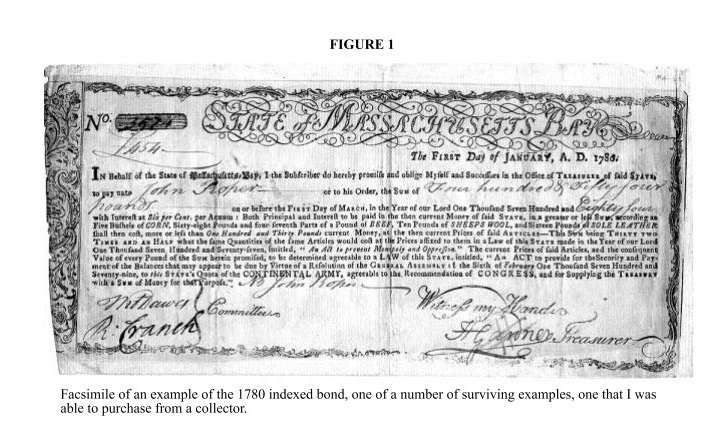

The Commonwealth of Massachusetts created the earliest known inflation-indexed bonds in 1780 in the Revolutionary War. Robert Shiller writes, "These bonds were invented to deal with severe wartime inflation and with angry discontent among soldiers in the U.S. Army with the decline in purchasing power of their pay. Although the bonds were successful, the concept of indexed bonds was abandoned after the immediate extreme inflationary environment passed, and largely forgotten until the twentieth century."

|

| Commonwealth of Massachusetts inflation-indexed bond, 1780, from Shiller (2003). |

"Both Principal and Interest to be paid in the then current Money of said STATE, in a greater or less SUM, according as Five Bushels of CORN, Sixty-eight Pounds and four-seventh Parts of a Pound of BEEF, Ten Pounds of SHEEPS WOOL, and Sixteen Pounds of SOLE LEATHER shall then cost, more or less than One Hundred and Thirty Pounds current money, at the then current Prices of said ARTICLES—This SUM being THIRTY-TWO TIMES AND AN HALF what the same Quantities of the same Articles would cost at the Prices affixed to them in the Law of this STATE made in the Year of our Lord One Thousand Seven Hundred and Seventy-seven, intitled, 'An Act to prevent Monopoly and Oppression.'"

Shiller explains that this historic episode is a good example of the role of economic theory in financial innovation. "John Maynard Keynes is widely quoted as asserting that most economic innovations derive ultimately from some 'academic scribblers.' But, in fact, in the case of indexed bonds, there was no academic precursor." He adds,

"It seems here that necessity was the mother of this invention. The example of the creation of indexed bonds in Massachusetts in 1780 appears to deny the importance of the “academic scribblers” that Keynes extolled, for the invention appeared long before the scholars wrote about it. And yet, in another sense, it only reinforces their importance, for the practice of indexation of bonds did not take hold at that time. It is a reasonable supposition that the indexed bonds did not continue because there was no well-conceived model that would justify and explain them."Certain developments in index number theory, for example, did not take place until the twentieth century. A simple price index like the one used on the 1780 bond has what is now a well-known problem. If the price of one of the goods rises, consumers can shift some of their consumption to other goods. Because of the ability to substitute, the increase in the price index is more than the increase in the true cost of living. Irving Fischer proposed a solution in 1922.

It wasn't until later in the twentieth century that inflation-indexed government bonds reappeared. This time around, academic scribblers abounded. The UK was a much earlier adopter than the US. On the recommendation of the Wilson Committee Report of 1980, then Chancellor of the Exchequer Geoffrey Howe announced the Government's intention to issue index-linked gilts.

Other countries, including Canada, Sweden, and New Zealand, followed in subsequent years. Whereas the high inflation in the Revolutionary War prompted inflation-indexed government debt, the high inflation in the US in the late 1970s did not have the same effect, at least not immediately. Shiller became one of the academic scribblers, coauthoring "A Scorecard for Indexed Government Debt" with John Campbell in 1996. Their scorecard came out in favor of creating inflation-indexed government debt. TIPS were introduced in 1997, and have since grown as a share of debt and of GDP (see figure below).

|

| Source: Campbell, Shiller, and Viceira 2009 |

(Since I'm writing about finance, I should add the disclaimer that this is not intended to be investment advice.)

This series looks to be awesome. Very interesting history of the Massachusetts security.

ReplyDeleteFor interest's sake, here's the story of where the Revolutionary War's inflation came from: http://www.mises.org/daily/2340

ReplyDeleteThe Massachusetts example is an interesting one.

ReplyDeleteArguably, though, by naming the UK, Canada, Sweden and New Zealand, but not Brazil you are still flattering the academic scribblers and underweighting necessity. Or is it your contention that the private measures taken to compensate for inflation in Brazil (which included not only indexing but also the practice of accruing interest only on business days, for example) owe a debt to academia?

EMERGENCY LOAN OFFER APPLY

ReplyDeleteWe Offer all types of Finance Business Personal Cash

Quick Cash Advance. Fast Credit Check. Cash Today.

Fast Cash Online

low interest rate as low as 2%

Financial Cash Available Here

Business Personal Cash

Solve Your Financial Problems

I'll advise All Cash seeker should contact us

THERE IS NOTHING TO LOSE BUT YOUR DEBT AND FINANCIAL PROBLEMS !!!

We Are Here To Show You A Better Way To Financial Freedom !!!

Contact Us At : abdullahibrahimlender@gmail.com

whatspp Number +918929490461

Mr Abdullah Ibrahim