In February, in response to questions by the House Financial Services Committee, Fed Chairman Ben Bernanke said that the asset purchase programs have not disrupted the markets for longer-term Treasuries or for mortgage-backed securities. The New York Fed followed up on this in the latest Survey of Primary Dealers, from March 2013. Primary dealers are trading counterparties of the New York Fed, and play an important role in implementing the asset purchase program. They are obligated to participate in open market operations and to provide the New York Fed's trading desk with market information and analysis. The primary dealers are surveyed each month to help the FOMC evaluate market expectations about the outlook for the economic and financial conditions and monetary policy.

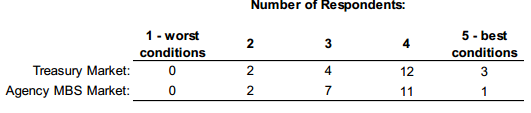

One question from the survey asked: How would you rate market functioning in longer-term Treasury and agency MBS securities markets today relative to the worst and best conditions you have seen since the beginning of 2009?

Here is a tabulation of the responses:

The survey also asked about expectations for the change in the amount of domestic securities held in the System Open Market Account (SOMA) portfolio over the next few years. I plotted the 25th, 50th, and 75th percentiles for expected cumulative changes in treasury holdings and in agency debt and MBS holdings below. Both types of asset holdings are expected to level off in the second half of 2014. But agency debt and MBS holdings are expected to start declining more quickly and rapidly than treasury holdings, which are expected to hold steady through the end of 2015 before beginning to decline.

Respondents were allowed to give written comments on their predictions:

"Some dealers assumed that future declines in the SOMA portfolio would be due to halting reinvestments only, while some dealers assumed halting reinvestments combined with sales. Several dealers expected such declines in the SOMA portfolio to occur at a fixed time before or after the first interest rate increase. Several dealers mentioned their views were based on the June 2011 exit principles while several others mentioned the FOMC will likely review its exit strategy, citing recent communication from Federal Reserve officials...

Some dealers expected sales of agency MBS securities to be a part of the exit strategy from accommodative policy. Some others thought that sales are unlikely or do not expect them to occur, with several mentioning that sufficient tightening could be brought about through other tools, including raising the interest rate paid on excess reserves (IOER) as well as temporary reserve draining."

Expected SOMA holdings at the end of 2014 are contingent on the level of unemployment by the end of this year. The blue bars show the probability distribution over holdings if the unemployment rate is less than 7.4% by the end of 2013. The red bars are if the unemployment rate is between 7.4 and 7.7%, and the green bars are if the unemployment rate is above 7.7%.

Very interesting post. Just wanted to mention that if you are interested in learning more about similar subject matter, in particular enterprise data model benefits, please check out the Modern Analytics website. They are the innovation leader when it comes to analyzing enterprise-level data.

ReplyDelete